If You Care About Inequality in America, Be Very Worried About What Trump Would Do to Health Care

A second Trump Administration could devastate Obamacare coverage relied upon by tens of millions of Americans, causing great harm to low-income working families

Much of the Biden campaign’s current focus is on Donald Trump’s many character flaws and general unfitness to lead our country. I trust that research by campaign professionals supports that these issues will affect the behavior of certain important categories of voters. But there must be a category of voters who, once they actually focus in on the election, will care about the things Donald Trump will do if he gains power again. Exposing his plans will be a big part of my work over the coming months (see Michelle Goldberg’s piece on abortion in the NYT this week and the Ezra Klein Show on tariffs as good examples of this kind of analysis).

Today I want to think about what Donald Trump, together with possible congressional majorities in both chambers of the Congress, would do to health care coverage in America. I am inspired to write about this after receiving a stunning email a couple of weeks ago:

The email got me thinking, yet again, about the privilege of having quality health insurance. Recovering from a disease, illness, or accident is hard enough as it is. The added burden of grappling with the staggering costs of health care if you are uninsured or have poor quality health coverage is unimaginable to me. But it is the reality for millions of Americans.

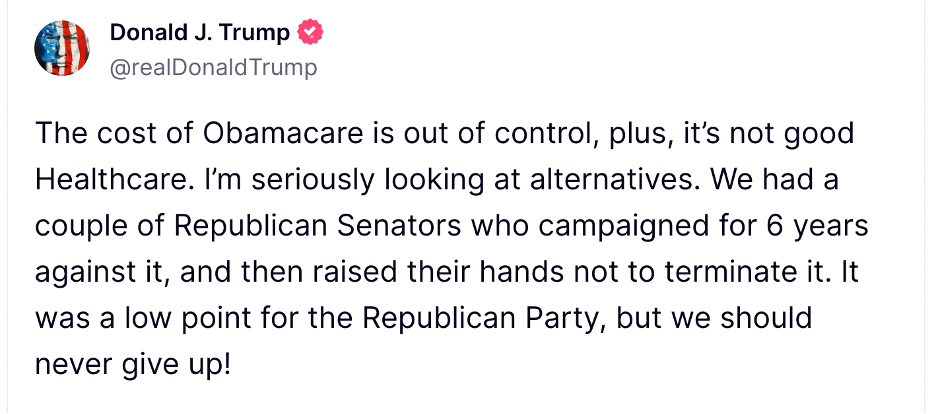

Last fall, Trump mused on Truth Social that if elected he would like to resurrect the failed effort during his presidency to repeal the Affordable Care Act (or “Obamacare”):

It personally goads Trump that he failed on this promise to voters, especially because a frequent target of Trump’s personal wrath, Senator John McCain, dramatically cast the final vote dooming the Obamacare repeal effort. Trump also gains great satisfaction undoing the legacy of another of his personal nemeses, Barack Obama. Trump is motivated by grudges much more than the nuances of policy. So, there are a great many reasons to believe that Trump’s Truth Social post accurately represents his true intentions.

That said, after the Biden campaign jumped on Trump’s threat to undo Obamacare, Trump attempted to moderate his position, stating that he was “not running to terminate Obamacare,” only that he would “make the A.C.A. much better than it is right now and less expensive for you.” This position echoes Trump’s statements during his presidency that he wanted to “repeal and replace” Obamacare with something better. Yet, the “repeal and replace” legislation that Trump helped get passed in the GOP-controlled House in 2017 was not “better” or “less expensive” for those in need of health care coverage. Indeed, it would have resulted in 17 million Americans immediately losing their Obamacare coverage and 32 million fewer people covered by 2026. The legislation to which John McCain famously gave a “thumbs down” would have cut the federal deficit by $473 billion, making it less expensive for the federal government, but far less generous to those in need of insurance. The Congressional Budget Office estimated that had Trump’s legislation passed, premiums for Obamacare policies would have risen by 25 percent by 2018, 50 percent by 2020, and 100 percent by 2026.

Those who rely on Obamacare for their health care insurance, or care about the American families and individuals who depend on this coverage, should not be at all reassured by Trump’s entirely political position that he is not running to repeal Obamacare. Trump’s campaign website contains no mention health insurance reform and his campaign has issued zero plans on how Trump would try to “improve” Obamacare. PolitiFact judges Biden’s statement that Trump wants to repeal the ACA “half true” in light of Trump’s contradictory statements and equivocation.

Another way to get some idea of what the health care insurance agenda might be during a second Trump agenda is to look to the ten, mostly-deep-red MAGA states that have chosen not to expand Medicaid under Obamacare (AL, FL, GA, KA, MS, TN, TX, SC, WI & WY). These states have an average uninsured rate double the rest of the nation. In these states, the median income threshold for Medicaid coverage is $9,812 for a family of three. This means that if you make over $10,000 a year, your family can’t enroll in Medicaid and does not qualify for any subsidy to purchase an Obamacare policy. Texas won’t even provide Medicaid coverage for a family of three that has income over $4,131! These states are satisfied with allowing approximately 1.5 million families with incomes substantially below the federal poverty line of $15,060 in annual income to go uninsured. (Note that Democratic governors in Kansas and Wisconsin have tried to expand Medicaid but been stymied by their GOP-controlled legislatures. Wisconsin’s Medicaid income threshold is six times higher than that of Texas, so at least it is providing coverage to some of the working poor in that state).

The policies implemented by these states is the kind of approach to health care insurance we can expect to spread nationally if Trump is elected and his MAGA followers take control of the key federal agencies in charge of Obamacare and federal Medicaid regulations. The notion that Trump and his MAGA acolytes will spend more federal dollars to reduce the health care cost for impoverished and very-low-income working poor families is, frankly, preposterous. If the past is prelude, what we are likely to see in a second Trump administration are efforts to pare back on Medicaid, cut subsidies that enable families to purchase Obamacare policies, and reduce federal oversight of the health insurance industry.

Obamacare is far from perfect, and could be improved upon, but Trump-led attempts to weaken or unravel it will have devastating impacts on millions of Americans.

Obamacare’s key achievement has been reducing the number of uninsured individuals and families. Due to Obamacare, the number of uninsured adults in the US dropped from the peak of 46.5 million in 2010 to 26.5 million by the end of Obama’s term in 2016. The number of uninsured then increased by two million people during the Trump years as his administration did virtually nothing to encourage people to sign up for coverage. But during the Biden administration, the uninsured rate is now at an all-time low of 7.7%. Enrollment in Obamacare policies hit a record high of 21 million in 2024.

Despite the advances under Obamacare, health care insurance remains extremely expensive and burdensome for many American families. Poor families get large subsidies to enable them to purchase insurance, but these policies often have extremely high deductibles, requiring payments of $5000 or more until full insurance benefits kick in. (To peruse policies available in the North Carolina Obamacare marketplace, see here.). Policies with lower deductibles are available, but of course the monthly premiums are substantially higher.

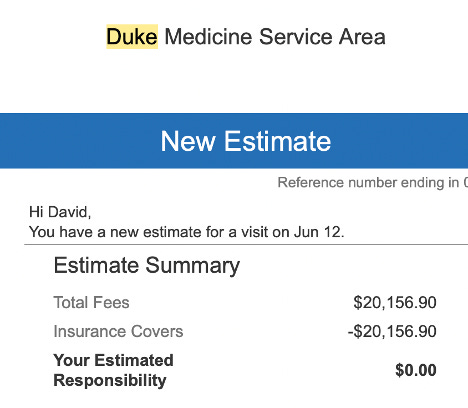

Having experienced large-scale health care expenditures myself this past 8 months, I was stunned to learn that Obamacare only limits out-of-pocket maximums to $9,450 per individual and $18,900 per family. This means that a poor or middle-income family with an Obamacare policy that has a family member facing a serious illness, a surgery, or expensive treatments may have to lay out almost $10K before that person’s health care needs are covered 100% by insurance. The out-of-pocket maximum on my employer-sponsored health insurance policy, in contrast, is $3,000, which is what led to me paying $0 on a $20,156 health care service I received earlier this month (noted in the email above).

So, even though Obamacare has improved our health care system substantially over the past decade by expanding coverage, most Americans are laying out a lot of money to pay for health care and even if they have insurance, they may face huge health care bills if they need anything but the most routine forms of care. It should come as no surprise that Americans now hold a staggering $220 billion in medical debt.

Given the vital importance of health care to every American, one would expect that the discussion during this election season would be about competing ideas on how to provide health insurance to the 25 million people in low-income working families who still do not have it and strengthening the quality of the policies that are currently sold in the Obamacare marketplaces. But we continue to have one candidate that rails against Obamacare, threatens to undo the progress that has been made over the past decade, and has no public plan to expand coverage or make health care insurance more affordable. The other candidate has an expansive health care agenda.

The choice should be clear for anyone that cares about addressing the deep inequalities in modern American society and the fundamental right to health care.